#20: Old wine in new bottle

Our history of labour welfare fund failures will repeat with the Rajasthan Gig Workers Act

In India, the number of gig workers is estimated to be around 7.7 million (in 2020-21) and is predicted to rise to 23.5 million by the year 2030 which would represent around ~4% of the workforce (NITI Aayog, 2022). However, gig workers are not covered by labour legislation in force.

This has led to demands for covering gig workers under labour welfare schemes and the Indian government has responded to the demands. Two new laws are expected to bring gig workers under labour welfare schemes: (i) The Code on Social Security, 2020 (by the Parliament of India), and (ii) The Rajasthan Platform Based Gig Workers (Registration and Welfare) Act, 2023 (by the legislature of Rajasthan). Rajasthan’s legislation has been hailed as a pioneering move to protect the interest of the gig workers (Hindustan Times, 2023).

However, this is not the first time that the Indian government has tried to create welfare legislation for a specific group of workers. The Rajasthan gig workers law follows the trend of many pieces of legislation, designed to provide security to workers in specific industries. This article analyses the outcomes of some labour welfare schemes and then compares them with private sector services that provide analogous services.

The article concludes by arguing that these laws generally fail, not because of poor implementation but because of incorrect fundamental principles. Economic theory (public choice) predicts that legislation like this is bound to fail because the interests of the workers are not aligned with the interests of the government officials appointed to protect them. No amount of administrative effort by the government will deliver the quality of welfare services that a private competitive market can provide. It may be far better to leave money in the hands of workers than to force a safety net.

Past legislation for workers

In India, governments have attempted to improve the lives of workers through legislation that targets a specific group of workers or through laws that apply in respect of a broad set of workers. The Rajasthan Gig Workers’ Act is similar to past legislation designed to protect specific groups of workers who do not fall under general labour law protection. Previously, the Parliament passed similar legislation to protect workers in mining, cinema, beedi, and construction since workers in these sectors were often informally employed. For example, Beedi factories are typically very small and may not come under the purview of the Factories Act, 1948. Similarly, construction sites can neither be classified as factories nor enterprises and therefore employment at such sites would be outside the scope of Factories Act or Shops and Establishments Act. Separately, state governments also attempted to bring a large set of workers under the purview of the regulations by enacting general labour welfare laws. The Labour Welfare Fund Acts are an example of such laws enacted at the state level.

These laws have a lot in common with each other. A Welfare Board is set up to carry out the welfare activities for workers. A tax/cess is imposed on the economic activity where these workers are employed. The revenue generated from the cess is spent on welfare activities for workers.

The table below shows how the Rajasthan Act is similar to one of the laws introduced in the past.

Broadly, the Welfare Board must perform three duties. First, the Board is required to identify and register workers as beneficiaries of various schemes. This is generally done by issuing identity cards to workers. Workers, once registered, can avail the benefits promised under those laws. Second, the Board is required to collect cess and fees. Typically, the cess collected from employers is the primary source of income for these Boards. A worker’s registration fee or subscription fee can also become an additional source of revenue for these Boards. Third, the Board is required to fund various welfare schemes designed for workers. These schemes relate to the provision of life or medical insurance, provision of pension, financial aid for housing, financial aid for the education of children, maternity benefits, etc.

The table below shows a list of laws introduced for different categories of workers and the forced contributions under them.

Legally, it is the employers who are required to pay the tax to the government. However, a part of that tax essentially comes out of the wages of the workers. This is because the tax increases the cost of doing business which can depress the wages of the workers. Therefore, a careful analysis is required to build a case for the utility of such labour welfare regulations.

Since general and sector-specific worker welfare legislation is not a new idea, we may be able to forecast the benefits of the Rajasthan Act by analysing how the other regulations have fared in benefiting their target communities. CAG audits, for instance, help cast light on the performance of worker welfare boards. The expenditure-to-income ratios of the Boards, claim settlement ratios, and other measures of efficiency such as trends in the registration of workers, magnitude of administrative expenses, etc. show that these laws have largely failed to meet the objective of improving the welfare of their intended worker segment.

Expenditure-to-Income Ratio

A primary way to measure the efficiency of welfare schemes is to look at expenditure-to-income ratios. This measure looks at what percentage of income received under the schemes was actually spent on welfare activities. The closer the expenditure is to the income, the more likely that workers are getting their money’s worth. Ideally, this ratio should be as close to one (100%) as possible. The ratio will never be one because there are always some administrative expenses for running any welfare scheme (like salaries of staff, rent for offices, record keeping expenses, etc). If this ratio is greater than one (for a long period), then it means that the welfare board will go bankrupt because the Board is spending more money than it is earning. Expenditure to income ratio much lower than one is also bad for workers. This implies that the Board is not spending money that has been collected for the welfare of the workers.

How do worker welfare boards perform in terms of expenditure-to-income ratio? The CAG has audited some of these boards in the past. The Fund for Construction Workers in Delhi was audited for the period of 2002-19, the fund for construction workers in Punjab was audited for the period 2013-19, and the funds for the Beedi, Cine, and Mine workers in eastern India were audited for the period of 2009-14. Similarly, annual reports of Labour Welfare Boards have been looked at for two states (Maharashtra and Karnataka) for doing this analysis. In terms of expenditure-to-income ratios, the results are depressing.

The table below shows the contrast between income received by Welfare Boards and expenditure incurred by the Welfare Boards/Labour Welfare Organisation.

For every Rs. 100 collected for construction workers in Delhi and Punjab, the workers only saw benefits worth Rs. 5 and Rs. 41 respectively. For Cine workers it was Rs. 14 and for mine workers it was Rs. 2. For workers in Maharashtra and Karnataka it was Rs. 42 and Rs. 16 respectively. Beedi workers were the only exception in this case who received benefits worth Rs. 104 for every Rs. 100 that was collected for them. However, this is also not sustainable since the Beedi welfare fund will eventually be exhausted.

What would have happened if this money had been invested in the market instead? Consider a hypothetical where the workers put this money in a bank fixed deposit. Banks are obligated to deploy (expend) all the funds (deposits) towards generating returns (welfare) of the investors (workers). If the hypothetical bank deposit generated a 9% return, the worker would have gotten Rs. 9 return, for a Rs. 100 deposit. The same Rs. 100 deposit at the same level of return would generate a return (benefits) worth Rs. 0.45 for construction workers in Delhi; Rs. 3.69 for construction workers in Punjab; Rs. 1.26 for cine workers; and Rs. 0.18 for mine workers; Rs. 3.78 for workers in Maharashtra and Rs. 1.44 for workers in Karnataka. Beedi workers would have gotten Rs. 9.36 but this is not sustainable since the Board would have gone bankrupt.

Claims settlement ratio

One head of expenditure for welfare boards is providing insurance to workers. For example, the Kolkata Labour Welfare Office (LWO) bought insurance for beedi workers from 2009-2014, from LIC. One way of measuring efficiency in life insurance schemes is to look at the claim settlement ratio, which measures the number of claims that are settled by the insurance provider against the number of claims that the insurance provider receives (in a year). As an illustration, suppose a life insurance provider receives 100 claims in a given financial year and the life insurer settles all 100 claims then the claim settlement ratio will be 100%. The closer the claim settlement ratio is to 100% the more efficient the insurance provider is considered.

The table below shows how the Kolkata Labour Welfare Office has performed in terms of honouring the life insurance claims forwarded by Beedi workers when compared with a few private life insurance providers.

Had the Beedi workers taken life insurance from a private company, they would have been better off. If 100 beedi workers had taken life insurance provided by the private sector, approximately 99 of them would have received the money from the private sector providers. In contrast, only 84 workers would receive the money through the Welfare Board. (We understand that this illustration ignores the premium discount the beedi workers may have gotten because of group buying. That being said, we don’t know the alternative insurance arrangements that may have emerged in the absence of the boards mediating.)

The efficiency of the board, as measured by the claim settlement, is probably an overestimation. This is due to poor documentation, as per the CAG, by the labour welfare office. The claim ratio was calculated assuming that all claims forwarded by the board (prior to 2013) were settled and the workers received the money they were owed. However, the CAG noted that the welfare board had no records of whether LIC actually paid out any of the insured, before 2013. The CAG could only establish that after 2013, none of the insured workers were paid. To be conservative, the calculation in this article assumes that all claims, before 2013, were paid by LIC (within a year). Therefore, the measure of 84% of claims being settled is the theoretical upper limit of the welfare board’s efficiency. If any claims before 2013 were not settled, the board’s efficiency would be even lower.

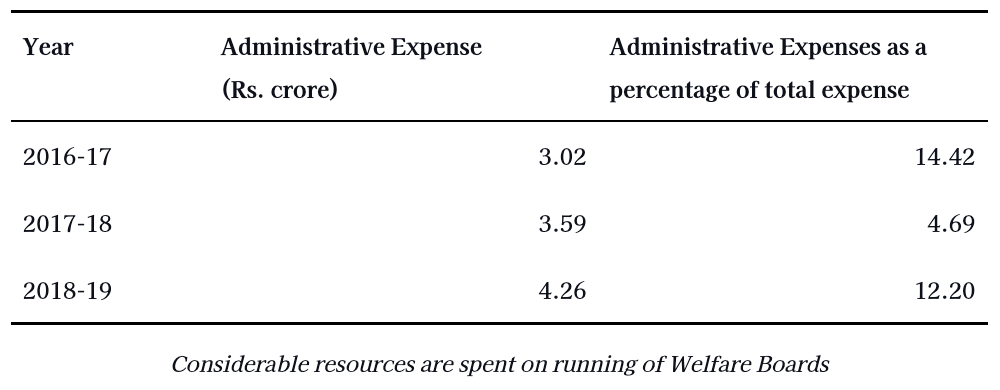

Administrative Expenses

Another way of measuring efficiency is by analysing the administrative expenses of welfare boards and private mutual funds. The administrative expenses are generally capped at a certain percentage of either the total expenditure of the total income of the fund through provisions laid down in the law. Labour Welfare Fund laws of states such as Maharashtra, Tamil Nadu and Karnataka have capped administrative expenses at a prescribed percentage of the total income of the fund. Similarly, section 24(3) of the Building and Other Construction Workers Act requires that

“No Board shall, in any financial year, incur... expenses exceeding five per cent. of its total expenses during that financial year.”

The audit revealed that the Board often failed to keep its administrative expenses below the stipulated limit. The table below shows the details of administrative expenses incurred by the Delhi Building and Construction Workers Welfare Board for the time period 2016 to 2019.

The total administrative expenses stood at Rs. 10.87 crore for a period of 2016-19. In two out of three financial years, the Board had exceeded the stipulated limit on administrative expenses set at 5 per cent of the total expenditure incurred during the year. This money could have been used for running the welfare schemes for construction workers. The audit revealed that the Board had not incurred any expenditure on 6 out of 15 welfare schemes during the same time period. Not only is the spending on actual welfare schemes low, but the proportion of the budget wasted on running day-to-day operations is also large.

In contrast, the workers would have been better off if they had invested in private-sector financial services. The securities regulator (SEBI) caps the administrative expenditure ratio to 2.25% for mutual funds. Therefore, for every Rs. 100 collected by the mutual fund, from investors, at least Rs. 97.75 is deployed in the market to generate returns for the investors. Another example of low administrative costs is the competitive market for pension funds in India where no pension fund in India charges more than 2% of the corpus as administrative costs.

Subscription

Another way to measure the quality of a social welfare scheme is to measure the number of persons willingly subscribing to such schemes. If participants see a benefit from the scheme, they will participate in them. However, this measure cannot be used for most of India’s labour welfare schemes because the schemes are not voluntary. The law requires employers and employees to participate in them. There is no opting out of ESIC, EPFO, or the schemes made for beedi workers, mine workers, etc. The only way workers or employers can opt out is by not registering with the Board. This is also not possible since registering the employers and employees is a basic activity of the Board. In fact, Rajasthan law requires employers (aggregators) to provide a database of all the onboarded workers with the state. Every employer is also required to get registered with the state (S.8 and S.9 of the Rajasthan Platform Based Gig Workers (Registration and Welfare) Act, 2023).

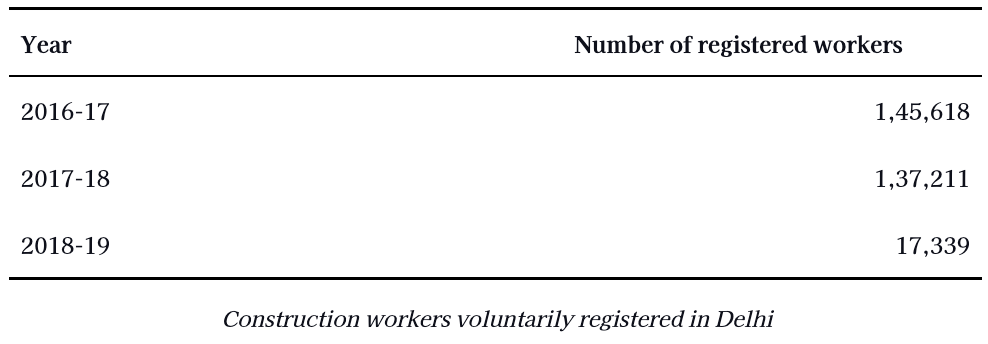

The Building and Other Construction Workers Act is an exception to the compulsory subscription model. A construction worker can cease to be a beneficiary due to non-payment of registration or subscription fee. The registration fees can differ for different states. For example, the rules made by Delhi require construction workers to voluntarily sign up for the benefits, and pay a small subscription fee of Rs. 25. Workers who did not pay this amount would not be entitled to the benefits under the law. This fee was not the primary source of funding the welfare schemes for construction workers in Delhi. The bulk of the money came from the cess that was collected on all building and construction work in Delhi.

Due to this setup, on paper, Delhi’s construction workers stood to gain a lot by paying the Rs. 25 subscription fee, as the bulk of the funds came from the cess. If a worker did not pay this amount, then such worker lost access to the funds collected from the builders. The table below shows the money collected from the workers (as subscription fees) and the cess collected from the builders in Delhi (for the years audited by CAG).

As the table above shows, workers should have got a great deal by voluntarily subscribing to Delhi’s construction welfare fund. This is because a worker (on paper) should have got benefits worth Rs. 22,727 by just contributing Rs. 25, a 909x benefit.

This calculation predicts that Delhi’s construction workers would be flocking to register with the welfare board. However, the observed participation rate was the opposite. The CAG recorded the membership for the three years as follows:

As the table above shows, during the audit period, Delhi’s construction welfare Board lost 88.09% of the workers. Similarly, Section 15 of the Tamil Nadu Labour Welfare Act requires every employer to contribute Rs. 20 per employee and every employee to contribute Rs. 10 to the Labour Welfare Fund. Data analysis shows that as the budget of the Tamil Nadu Labour Welfare Board increased between 2014 and 2019, the number of beneficiaries actually reduced. This indicates that workers do not value the services that the Welfare Boards are providing. Any private service provider would have gone bankrupt with this level of performance.

Other issues

Other failings include laxity in maintaining proper financial records, delay in payment of scholarships to children, and exclusion of beneficiaries. For example, the CAG report found that the Delhi Building and Construction Welfare Board had never prepared a budget since its inception and were lax in maintaining proper books of accounts during the audit years, contravening the provisions of the Act. Similarly, the labour office in Kolkata delayed the sanctioning of scholarships provided to children of workers by a year affecting the education of 1.06 lakh children due to unavailability of timely budgets. Consequently, it is not clear how many children were able to continue their education due to untimely payment of scholarships. The Board has also been selective about identifying beneficiaries. For instance, it was found that out of 144 districts that the labour office is in charge of, payments were made to beneficiaries belonging to just 4 districts. That is, the labour office covered approximately 3% of the total districts that come under their purview.

Conclusion

Following Rajasthan, it is expected that many other states will introduce schemes or legislation intended to benefit gig workers (The Wire, 2023). However, history shows that protecting the interests of the workers through legislation has not worked well. The laws that are likely to be introduced in the future may go down the same path as other worker welfare regulations in the past.

It is tempting to believe that the labour welfare laws are good in principle but fail due to poor administration. If only we had good/hard-working labour officers we could have had a situation where workers would have benefited from various welfare schemes from these laws.

This thinking is incorrect. It is not that these laws are well thought out and that labour officers are incompetent. Rather, these laws are incorrectly conceptualised and no amount of additional effort can improve outcomes for workers. This is because the central feature of these laws is creating a government board that takes financial decisions on behalf of the workers. This government body faces no accountability in fund collection and no incentives in fund deployment.

In contrast to unaccountable government boards, private service providers have to compete with each other to acquire the services of customers. Instead of relying on the state to solve the problem of the absence of markets in the case of some workers, an alternative approach could be to deepen our financial markets such that a large class of workers are able to have access to financial market services. This will allow the workers the freedom to plan their own welfare bypassing the inefficient government agency.

Besides the inefficient use of funds collected, gig workers may further be harmed by the introduction of such laws since these laws can increase the cost of operations for platform-based aggregators. The gig economy has flourished due to the flexible and dynamic nature of the work arrangement between aggregators and gig workers. Laws that undertake to promote gig worker welfare may in fact make these arrangements less attractive and cost us jobs.

References

Code on Social Security (2020). https://www.indiacode.nic.in/bitstream/123456789/16823/1/a2020-36.pdf

Hindustan Times. (2023, October 17). Gig workers law deepens industrial democracy. Hindustan Times. https://www.hindustantimes.com/opinion/gig-workers-law-deepens-industrial-democracy-101697552323915.html

NITI Aayog. (2022). India’s Booming Gig and Platform Economy: Perspectives and Recommendations on the Future of Work. https://www.niti.gov.in/sites/default/files/2022-06/25th_June_Final_Report_27062022.pdf

The Building and Other Construction Workers’ Welfare Cess Act (1996). https://www.indiacode.nic.in/bitstream/123456789/1948/1/A1996__28.pdf

The Rajasthan Platform Based Gig Workers (Registration And Welfare) Act (2023). https://prsindia.org/files/bills_acts/acts_states/rajasthan/2023/Act29of2023Rajasthan.pdf

The Wire. (2023, November 14). Ahead of Telangana Elections, Gig Workers’ Union Demands a Rajasthan-Like Welfare Law. The Wire. https://thewire.in/rights/ahead-of-telangana-elections-gig-workers-union-demands-a-rajasthan-like-welfare-law

Bhuvana Anand, Suyog Dandekar and Shubho Roy are researchers at Prosperiti.